Buying a Home in Calabasas as an Investor

Calabasas 91302 and 91372 are not a BRRRR market. Investors who arrive expecting the Lake Balboa or Reseda playbook — acquire below comp ceiling, execute a focused renovation, refinance to recover capital, repeat — will find that Calabasas's $1.3M–$2.5M+ entry price, its premium-finish buyer expectation, and its Las Virgenes Unified School District demand anchor produce a fundamentally different investment thesis. This is an appreciation-and-rental-yield market built on school quality durability, Mello-Roos-financed master-planned infrastructure, and a buyer pool with the income depth to sustain values through rate cycles that compress more price-sensitive SFV markets.

That doesn't make Calabasas a weaker investment market — it makes it a different one, with its own specific mechanics, its own specific risks (wildfire insurance exposure chief among them), and its own specific opportunities (the LVUSD rental premium, the long-hold appreciation case, the limited but real renovation arbitrage in original-condition older-stock pockets). This article gives investors the complete Calabasas framework: the investment case, the realistic financial model at current rates, the specific due diligence items this market requires that the central Valley doesn't, and the honest assessment of who should and shouldn't deploy capital here.

1. 📊 The Calabasas Investment Case — Why This Market, Why Now

The investment case for Calabasas 91302 and 91372 rests on a different foundation than the central Valley markets in the PEP coverage area. It is built less on acquisition discount and renovation lift, and more on demand durability, rental rate ceiling, and the specific appreciation pattern that a planned, school-anchored, geography-constrained community produces over a long hold.

Calabasas 91302's established luxury housing stock — the product type that anchors the buy-and-hold investment thesis here. Unlike the central Valley's renovation-arbitrage opportunity, Calabasas investment returns are driven primarily by LVUSD-anchored demand durability and long-run appreciation rather than forced equity creation through cosmetic improvement.

Calabasas 91302's established luxury housing stock — the product type that anchors the buy-and-hold investment thesis here. Unlike the central Valley's renovation-arbitrage opportunity, Calabasas investment returns are driven primarily by LVUSD-anchored demand durability and long-run appreciation rather than forced equity creation through cosmetic improvement.

Fundamental 1 — The LVUSD demand floor is the strongest school-quality anchor in the coverage area:

Las Virgenes Unified School District consistently outperforms LAUSD on measured academic outcomes across the district's elementary, middle, and high schools serving Calabasas. This is not a single-school premium the way Granada Hills Charter or El Camino Real function in their respective markets — it is a district-wide reputation that affects every Calabasas address, producing:

- → A rental and resale demand floor that holds during rate cycles that suppress discretionary luxury demand elsewhere

- → A tenant pool willing to sign longer leases and pay rental premiums specifically to establish LVUSD residency for their children, producing lower turnover and more predictable occupancy than comparable-priced rentals without a school anchor

- → Resale buyer depth that has proven durable through the 2022–2023 correction — LVUSD-zone Calabasas properties retraced less and recovered faster than comparable non-school-anchored luxury SFV inventory

Fundamental 2 — The buyer and renter pool has income depth that rate cycles don't fully suppress:

Calabasas's resident population skews toward entertainment industry executives, business owners, and professionals with income and asset profiles that absorb elevated rates more comfortably than the central Valley's rate-sensitive buyer pool. This doesn't make Calabasas immune to rate effects — premium-tier DOM has extended in 2026 just as it has in Studio City and Granada Hills — but it does mean the demand floor under any given Calabasas address is deeper than in markets where qualification is the binding constraint for most buyers.

Fundamental 3 — Geographic constraint limits new supply:

Calabasas's position within the Santa Monica Mountains foothills and the specific land-use and development constraints that mountain-interface communities operate under mean that new single-family supply is limited relative to demand. This is the same dynamic that supports long-run appreciation in Topanga, the Hollywood Hills, and other geographically constrained luxury markets — scarcity of buildable land sustains pricing power in a way that flatter, more developable central Valley geography doesn't replicate.

Fundamental 4 — Mello-Roos-financed infrastructure sustains community quality without ongoing capital calls on the investor:

Significant portions of Calabasas — particularly newer development within the master-planned sections of 91302 — were built using Mello-Roos Community Facilities District financing, which funded the parks, the road infrastructure, and the community amenities through a special tax assessment on the original developments rather than through HOA special assessments that can hit investor-owners unpredictably. Investors should understand which specific Calabasas properties carry Mello-Roos obligations (verify through the preliminary title report and NHD disclosure) — these add a fixed, predictable annual cost rather than the variable capital-call risk that some non-Mello-Roos HOA communities carry.

2. 🏠 The Buy-and-Hold Strategy in Calabasas — Why BRRRR Doesn't Work Here

Understanding why BRRRR fails in Calabasas is as important for investor decision-making as understanding what does work — because investors who attempt to apply the central Valley playbook here will misallocate capital against a market structure that doesn't support it.

Why the BRRRR math breaks down at Calabasas price points:

The BRRRR strategy depends on a specific relationship: acquisition price plus renovation cost must land at or below approximately 75% of post-renovation appraised value, so that a cash-out refinance recovers most or all invested capital. In Lake Balboa or Reseda, this works because:

- → The gap between original-condition and renovated comp ceilings is large relative to acquisition price (often 25-35%)

- → Renovation costs are modest relative to the comp ceiling (a $45,000–$65,000 focused scope against an $800K-$900K ceiling)

- → A meaningful supply of original-condition inventory exists at prices that support the 75% LTV math

In Calabasas, none of these three conditions holds reliably:

- → ⚠️ The condition gap is smaller in percentage terms: Most Calabasas housing stock is already well-maintained or recently updated — the buyer and seller pool at this price point doesn't tolerate the deferred maintenance that produces large value gaps in working-family markets. Original-condition Calabasas inventory at a meaningful discount to renovated comps is rare specifically because long-term Calabasas owners have generally kept their properties at a presentation standard the market expects.

- → ⚠️ Renovation costs scale up disproportionately: A Calabasas-appropriate kitchen and bath renovation that satisfies the buyer expectation at this price point runs $120,000–$220,000 — not the $45,000–$65,000 focused scope that works in the central Valley. The renovation cost consumes a much larger share of any comp gap that does exist.

- → ⚠️ The thin acquisition opportunity: Finding a genuinely below-market Calabasas acquisition requires extended DOM, estate sales, or distressed situations — and at this price point, those situations are infrequent and heavily competed for by both retail buyers and other investors.

What does work — the buy-and-hold rental model:

The Calabasas investment thesis that actually produces returns is straightforward: acquire a well-positioned, move-in-ready or lightly-updated single-family home in an LVUSD-strong sub-neighborhood, hold it as a long-term rental to the school-motivated tenant pool, and let appreciation and rental income compound over a 7-15 year hold rather than attempting to force equity through renovation and rapid capital recycling.

- → ✅ Target condition: Move-in-ready to lightly dated — not original-condition fixer inventory. The Calabasas tenant pool at $6,000–$9,500/month rent expects quality finishes; a property requiring renovation before it can command premium rent sits vacant longer and erodes the return.

- → ✅ Target sub-neighborhood: LVUSD-verified addresses with elementary, middle, and high school assignment confirmed through lvusd.org and direct district contact — the school anchor is the rental demand driver and must be verified, not assumed

- → ✅ Target hold period: 7-15 years minimum. Calabasas investment returns are a long-run appreciation and rental-yield story, not a 12-24 month flip or BRRRR cycle

3. 💰 The Calabasas Investment Financial Model — Real Numbers for 2026

This section builds the complete financial model for a Calabasas 91302 buy-and-hold investment at current market conditions — acquisition, financing, rental income, expenses, and the honest return picture that reflects this market's actual mechanics rather than borrowed central-Valley assumptions.

This section builds the complete financial model for a Calabasas 91302 buy-and-hold investment at current market conditions — acquisition, financing, rental income, expenses, and the honest return picture that reflects this market's actual mechanics rather than borrowed central-Valley assumptions.

The base case Calabasas investment:

Acquisition:

- → Purchase price: $1,650,000 (a representative core Calabasas 91302 single-family home, 4-bedroom, well-maintained, LVUSD-verified)

- → Down payment (25% investor financing): $412,500

- → Closing costs: $24,000

- → Total acquisition cash deployed: $436,500

Financing:

- → Loan amount: $1,237,500 at 7.25% (investor rate, 30-year)

- → Monthly P&I: $8,438

Monthly expenses:

- → Property taxes (1.0% base + Mello-Roos if applicable + LA County assessments, estimated 1.2% effective): $1,650/month

- → Insurance — see Section 5 for the critical wildfire insurance discussion; estimated $550–$1,100/month depending on specific address and FAIR Plan dependency

- → Property management (8% of gross rent): $560–$680/month

- → Maintenance reserve (1% annually on value): $1,375/month

- → HOA dues (if applicable — verify per specific address): $0–$450/month

- → Total monthly expenses: approximately $4,135–$5,235 (excluding HOA)

Rental income:

- → Monthly rent (4-bedroom, well-maintained, LVUSD-verified, 91302 core sub-neighborhood): $7,000–$8,500/month

Monthly cash flow:

- → $7,750 (rent midpoint) - $8,438 (P&I) - $4,685 (expenses midpoint) = -$5,373/month

The honest cash flow assessment:

This is a significantly negative monthly cash flow position at current financing rates — more negative in absolute dollar terms than the central Valley examples in prior PEP investor articles, because the loan amount and the expense base are both proportionally larger. This is the single most important number for any prospective Calabasas investor to internalize before proceeding: at 2026 rates, a leveraged Calabasas single-family rental does not cash-flow positive on a monthly basis for most investors. The return case here is built on appreciation and equity buildup, not monthly income.

The annual return with appreciation:

- → Monthly negative cash flow: -$5,373 × 12 = -$64,476 annual cash drain

- → Annual appreciation at 5% on $1,650,000 (Calabasas's stronger historical appreciation rate relative to central Valley): +$82,500

- → Principal paydown (year one, approximate): +$13,200

- → Net annual wealth building: approximately +$31,224

This is a positive total-return outcome, but it requires the investor to fund a substantial annual cash drain from outside reserves — approximately $64,500/year, or roughly $5,400/month, that must come from the investor's other income or liquid capital, not from the property's own performance. This is fundamentally different from the central Valley investor profile, where the cash drain is in the $2,500-$3,000/month range and far more sustainable for a mid-level investor without significant outside income.

Who this math works for:

- → ✅ High-income investors (typically $400,000+ household income or substantial liquid investment capital) who can comfortably absorb a $60,000-$70,000 annual carrying cost as a long-term wealth-building strategy

- → ✅ Investors with a genuine 10+ year hold horizon who are underwriting the investment on appreciation and eventual mortgage payoff, not near-term cash flow

- → ✅ 1031 exchange buyers moving equity out of a lower-appreciation asset into Calabasas's stronger long-run appreciation profile, where the exchange defers tax on existing gains and the new asset's appreciation trajectory is the primary investment thesis

The rate sensitivity:

If rates moderate from 7.25% to 6.0%:

- → Monthly P&I on $1,237,500 drops to approximately $7,420 — a $1,018/month improvement

- → Revised monthly cash flow: approximately -$4,355/month

- → Still negative, but a meaningfully smaller annual drain (-$52,260 versus -$64,476)

Rate relief helps this math but doesn't transform it into a cash-flow-positive proposition at Calabasas price points without either a larger down payment (40%+) or the addition of rental income from an ADU or guest unit where the property and HOA permit it.

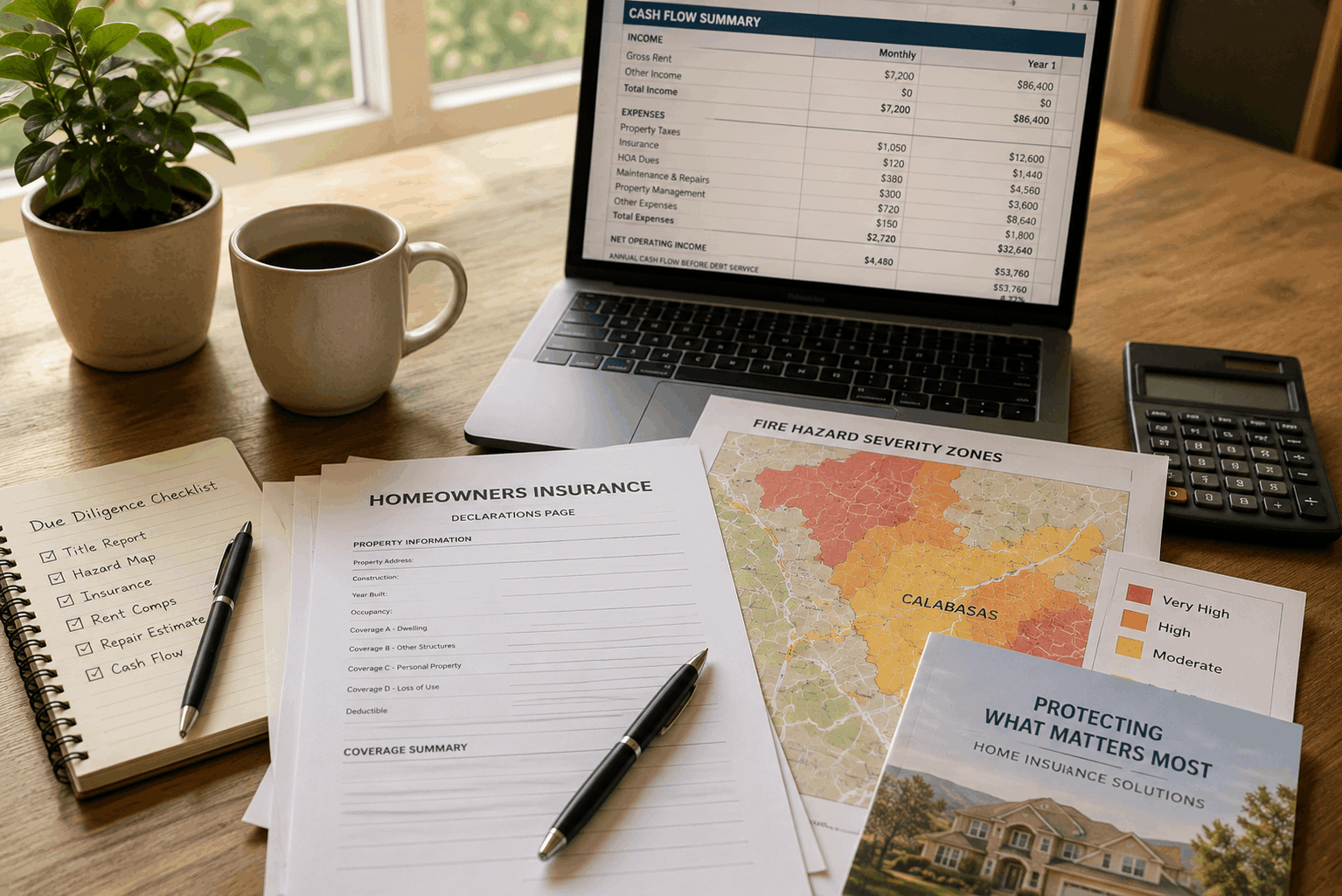

4. 🔍 Calabasas-Specific Due Diligence — What This Market Requires That the Central Valley Doesn't

Investor due diligence in Calabasas requires attention to a specific set of items that either don't exist or are far less consequential in central Valley markets like Lake Balboa or Reseda.

Wildfire insurance due diligence — the single most consequential underwriting variable for a Calabasas 91302/91372 investment property in 2026. Verifying binding insurance availability and cost before closing, rather than after, is the difference between a financial model that holds and one that collapses under an unanticipated FAIR Plan premium.

Wildfire insurance due diligence — the single most consequential underwriting variable for a Calabasas 91302/91372 investment property in 2026. Verifying binding insurance availability and cost before closing, rather than after, is the difference between a financial model that holds and one that collapses under an unanticipated FAIR Plan premium.

✅ Wildfire insurance and Fire Hazard Severity Zone status — the critical Calabasas variable:

This is the due diligence item that most distinguishes Calabasas investing from the central Valley, and the one investors most consistently underestimate:

- → 🔥 Verify Very High Fire Hazard Severity Zone (VHFHSZ) status for every specific address through the Cal Fire FHSZ viewer before making any offer. Significant portions of Calabasas — particularly the hillside and Santa Monica Mountains-interface sub-neighborhoods — carry VHFHSZ designation.

- → 🏠 Obtain binding insurance quotes during the inspection period, not after closing. Multiple major carriers have reduced or eliminated new-policy underwriting in California's highest fire-risk zones. For VHFHSZ Calabasas properties, the California FAIR Plan (the state's insurer of last resort) may be the only available option, and FAIR Plan premiums for a $1.5M-$2.5M Calabasas home can run $4,500-$11,000+ annually — a figure that materially changes the monthly cash flow model above.

- → 📋 Model your investment using the actual FAIR Plan quote, not a generic insurance assumption. An investor who underwrites a deal assuming $4,000/year in insurance and discovers a $9,500/year FAIR Plan requirement post-close has changed their annual cash drain by $5,500 — a material swing in a model that was already cash-flow negative.

- → 🌲 Evaluate defensible space and brush clearance requirements — VHFHSZ properties have specific ongoing maintenance obligations that affect the rental property's operating cost and the landlord's liability exposure if not maintained to code.

✅ Mello-Roos and special assessment verification:

- → 📝 Pull the preliminary title report and NHD disclosure to identify any Mello-Roos Community Facilities District obligations specific to the address — these appear as a fixed annual line item on the property tax bill and should be incorporated into the expense model as a known, predictable cost rather than discovered after close.

- → 🏛️ Verify HOA status and dues for any Calabasas property in a planned community or gated development — confirm current dues, any pending special assessments, and the HOA's reserve fund health through the HOA's financial documents, which sellers are obligated to provide during escrow.

✅ LVUSD enrollment verification — non-negotiable for the rental thesis:

- → 🏫 Verify the specific elementary, middle, and high school assignment for any target address through lvusd.org and direct district contact before underwriting the LVUSD rental premium into your pro forma. LVUSD boundaries include some addresses that are technically Calabasas but fall into different school assignments — confirm precisely.

- → 📊 Recognize that the LVUSD premium is most valuable to school-age-family tenants specifically — a 2-bedroom condo or a property without family-appropriate floor plan won't capture the same rental premium that a 4-bedroom single-family home in a verified LVUSD catchment commands.

✅ Geological and hillside-specific inspection (where applicable):

- → 🌋 Order a geotechnical inspection for any Calabasas property on a slope or in a hillside sub-neighborhood — slope stability, retaining wall condition, and drainage are material to both safety and long-term capital expenditure planning, exactly as in the hillside sub-neighborhoods of Granada Hills 91344 but with higher absolute dollar stakes given Calabasas price points.

✅ Permit history review:

- → 📋 Pull the City of Calabasas permit history for the specific address — verify that any additions, pool installations, or structural modifications have corresponding permits. Unpermitted work is a more consequential discovery at $1.5M-$2.5M price points than at central Valley prices, both in absolute remediation cost and in the financing and insurance complications it can create.

5. 🏘️ Where to Invest Within Calabasas — Sub-Neighborhood Analysis for Investors

Calabasas 91302 and 91372 are not uniform investment markets. Sub-neighborhood selection determines acquisition price, LVUSD certainty, rental rate ceiling, and the wildfire insurance exposure that has become a central underwriting variable.

Calabasas 91302's core established flatland sub-neighborhoods — generally lower Fire Hazard Severity Zone exposure than the hillside-interface streets, more straightforward insurance underwriting, and the most accessible entry point for investors prioritizing predictable cash flow modeling over hillside view premiums.

Sub-neighborhood 1 — Core established flatland streets (lower fire risk tier):

- → 📊 Acquisition range: $1.3M-$1.7M for well-maintained 3-4 bedroom homes

- → 🔥 Fire risk profile: Generally lower VHFHSZ exposure than hillside-interface streets — verify per address, but this tier typically presents more straightforward, more available, and less expensive insurance underwriting

- → 🏫 LVUSD certainty: Strong — most core flatland addresses fall clearly within well-established LVUSD elementary and middle school catchments

- → 💰 Rental rate: $6,200-$7,500/month for a well-maintained 3-4 bedroom home

- → 📍 Investor case: The most straightforward Calabasas entry point — predictable insurance, strong LVUSD certainty, and the rental tenant pool depth that comes with proximity to the Calabasas Commons and core community infrastructure

Sub-neighborhood 2 — Calabasas Park-adjacent and lake-proximate streets:

- → 📊 Acquisition range: $1.5M-$2.0M

- → 🏞️ Investment case: Proximity to Calabasas Lake and the community park anchor commands a lifestyle premium that supports both stronger resale value and a rental premium from tenants specifically seeking the walkable family-park access

- → 💰 Rental rate: $6,800-$8,200/month

Sub-neighborhood 3 — Hillside and Santa Monica Mountains-interface streets (premium and higher-risk tier):

- → 📊 Acquisition range: $1.8M-$2.5M+, with view-premium properties extending higher

- → 🔥 Fire risk profile: Meaningfully higher VHFHSZ exposure — this is where the insurance due diligence in Section 4 is most consequential. Some addresses in this tier may be FAIR-Plan-dependent, materially changing the investment math.

- → 🏔️ Investment case: The view and privacy premium can support strong rents and resale values for investors who have done the insurance underwriting correctly — but this is the tier where an investor who skips the binding insurance quote step is most likely to discover their model doesn't hold

- → 💰 Rental rate: $7,500-$10,500+/month for premium view properties, reflecting the executive and entertainment-industry tenant pool this tier specifically attracts

Sub-neighborhood 4 — 91372 (smaller zip code, generally newer/master-planned sections):

- → 📊 Acquisition range: $1.4M-$2.2M depending on specific development

- → 🏛️ Mello-Roos consideration: Newer master-planned sections of 91372 are more likely to carry Mello-Roos obligations — verify the specific fixed annual cost and incorporate it into the expense model

- → 💰 Rental rate: $6,500-$8,500/month

🚫 What NOT to Overdo

Don't apply the central Valley BRRRR framework to a Calabasas acquisition. The single most consequential mistake an investor can make in this market is assuming the renovation-arbitrage math that works in Lake Balboa or Reseda will work here. The comp gaps are smaller, the renovation costs scale up disproportionately to the price point, and the available original-condition inventory at acquisition-discount prices is rare. If your investment thesis depends on a cash-out refinance recovering most of your invested capital within 12-18 months, Calabasas is not the right market for that capital.

Don't underwrite a Calabasas investment without a binding wildfire insurance quote in hand. This is not a generic disclaimer — it is the specific underwriting failure that has changed multiple investor pro formas from cash-flow-manageable to cash-flow-untenable after close. A model built on an assumed $4,500/year insurance cost that turns into a $9,800/year FAIR Plan premium has absorbed an unplanned $440/month hit to an already negative cash flow position. Get the quote during the inspection period, before you remove contingencies, every time.

Don't assume every Calabasas address carries the same LVUSD premium. The school-quality rental and resale premium that anchors this market's investment thesis is address-specific, not blanket-applicable to anything with a Calabasas mailing address. Verify enrollment eligibility through lvusd.org and direct district contact for every target property — an address that turns out to be outside the strongest LVUSD catchments, or that feeds to a less sought-after school within the district, won't command the same rental premium your pro forma may assume.

Don't deploy Calabasas-level capital without genuine 7-15 year hold commitment. The negative monthly cash flow that characterizes most leveraged Calabasas acquisitions at current rates is a position an investor needs to be able to sustain for years, not months, before appreciation and principal paydown produce the total return that makes the investment worthwhile. Investors who need liquidity within 2-3 years, or whose other income is not stable enough to reliably absorb a $50,000-$70,000 annual carrying cost, should look toward the central Valley's more cash-flow-forgiving markets instead.

Don't ignore HOA reserve fund health and pending special assessments in gated or planned communities. Several Calabasas sub-neighborhoods operate within HOA-governed communities with shared amenities — pools, gates, landscaped common areas — that require ongoing reserve funding. An HOA with a poorly funded reserve is a special-assessment risk that can hit an investor-owner without warning. Review the HOA's financial statements and reserve study during escrow, not after closing.

🏠 Real-World Scenario — Calabasas 91302

An investor with a successful Sherman Oaks 91403 rental portfolio and approximately $550,000 in available capital from a recent 1031 exchange was evaluating whether to deploy into a fourth central Valley property or diversify into Calabasas. His existing portfolio cash-flowed modestly positive across three properties acquired at lower price points pre-2022.

We ran the honest comparison. A fourth central Valley acquisition at $850,000 would likely produce modest positive cash flow consistent with his existing portfolio — a familiar, lower-risk continuation of his existing strategy. A Calabasas 91302 acquisition at $1.65M would produce a meaningfully negative monthly cash flow position (consistent with the base case model above) that his existing rental income could not fully absorb without dipping into his other income sources.

We walked through the LVUSD demand durability case and the appreciation differential — Calabasas's 5-6% historical annual appreciation versus the 3.5-4% he had experienced in his central Valley holdings — and the specific risk that a Calabasas acquisition required: verified binding insurance, confirmed LVUSD catchment, and a genuine willingness to fund a $5,000+/month carrying cost from his W-2 income for the foreseeable holding period.

He chose to split the capital: $300,000 into a Calabasas 91302 acquisition in the core flatland tier (lower insurance risk, strong LVUSD certainty) using additional financing to complete the purchase, accepting the negative cash flow as a long-term appreciation play funded partly by his stable employment income, and the remaining $250,000 into a fourth central Valley property that preserved his portfolio's cash-flow character. Eighteen months in, the Calabasas property has appreciated approximately 7% and rents to an LVUSD-motivated family at $7,200/month; the cash flow remains negative as modeled, funded as planned from his other income, with no surprises because the insurance quote was obtained and the school catchment verified before closing.

🏠 Real-World Scenario — Calabasas 91302

A physician couple with significant liquid capital from a medical practice sale were considering a $2.1M Calabasas 91302 hillside property with mountain views — drawn specifically to the premium tier described in Section 5. The listing agent's marketing materials did not mention Fire Hazard Severity Zone status.

We pulled the Cal Fire FHSZ viewer for the specific address before any offer: Very High Fire Hazard Severity Zone, confirmed. We advised obtaining a binding insurance quote before submitting an offer rather than during the inspection period, given the property's price point and the couple's intention to hold it as a long-term rental rather than owner-occupy.

The quote process took three weeks and required two carrier rejections before a FAIR Plan quote was secured: $9,400 annually for fire coverage, supplemented by a separate difference-in-conditions policy for liability and other perils, bringing total annual insurance cost to approximately $12,100 — nearly three times the $4,200 the couple had initially budgeted based on a generic regional insurance estimate.

We rebuilt the financial model with the actual quote. Monthly cash flow moved from an initially modeled -$6,100/month to -$6,775/month — a $675/month, $8,100/year difference that the couple needed to consciously accept before proceeding. They had the capital depth to absorb it and valued the specific mountain-view premium and rental ceiling ($9,200/month achieved) enough to proceed with full information.

The couple closed with accurate numbers and no post-close insurance surprise. A different investor who skipped the pre-offer insurance verification step on this same property — as happens regularly in this market — would have discovered the $12,100 annual premium only after removing contingencies, with meaningfully less leverage to walk away or renegotiate.

❓ FAQ

Is Calabasas a good place to invest in real estate? For investors with substantial capital depth, a genuine long-hold horizon (7-15 years), and the ability to fund a significant negative monthly cash flow from outside income or reserves — yes, primarily as an appreciation and LVUSD-anchored rental-demand play rather than a near-term cash-flow or renovation-arbitrage strategy. Calabasas 91302 and 91372 are not the right market for investors seeking BRRRR-style capital recycling or near-term positive cash flow; they are a strong fit for investors diversifying into a school-quality-anchored, geographically constrained luxury market with a demonstrated history of appreciation durability through rate cycles.

Does BRRRR work in Calabasas? Generally no, not in the way it works in the central Valley. The comp gap between original-condition and renovated Calabasas inventory is smaller in percentage terms than in markets like Lake Balboa or Reseda, renovation costs scale up disproportionately to satisfy the buyer-expectation finish quality at this price point, and genuinely below-market original-condition acquisitions are rare and heavily competed for. Investors specifically seeking BRRRR mechanics should look to the central Valley markets in the PEP coverage area rather than Calabasas.

What is the rental income on a Calabasas investment property? Rental rates for well-maintained single-family homes in Calabasas 91302/91372 in 2026: ✓ Core flatland 3-4 bedroom: $6,200-$7,500/month. ✓ Calabasas Park/lake-adjacent: $6,800-$8,200/month. ✓ Premium hillside/view properties: $7,500-$10,500+/month. These rates assume verified LVUSD catchment and move-in-ready to lightly-updated condition — original-condition or non-LVUSD-verified properties command meaningfully less. Verify current comps through active rental listings for your specific sub-neighborhood before building assumptions into a pro forma.

Why is wildfire insurance such a big deal for Calabasas investors? Significant portions of Calabasas, particularly hillside and Santa Monica Mountains-interface sub-neighborhoods, are designated Very High Fire Hazard Severity Zones by Cal Fire. Multiple major insurance carriers have reduced or eliminated new-policy underwriting in California's highest-risk zones, leaving the California FAIR Plan (the state's insurer of last resort) as the only available option for many properties — at premiums that can run $4,500-$12,000+ annually depending on the specific address and coverage needs. Because this single line item can represent several hundred dollars of monthly cash flow difference, it must be verified with a binding quote before closing rather than estimated.

Does Calabasas have ADU potential for investors? ADU opportunity in Calabasas is more limited than in central Valley markets like Lake Balboa. Many Calabasas properties sit within HOA-governed or gated communities with CC&Rs that restrict or prohibit ADU construction regardless of state ADU legislation, and existing homes are frequently larger relative to lot size than central Valley equivalents, leaving less practical room for a detached unit. Verify HOA restrictions and specific lot configuration before assuming ADU income into any Calabasas investment model — this is not the reliable value-add lever here that it is in Lake Balboa 91406/91411.

How much capital do I need to invest in Calabasas real estate? At 2026 prices and rates, plan for $400,000-$700,000+ in deployable capital for a single leveraged acquisition: approximately $325,000-$625,000 for a 25% down payment plus closing costs on a $1.3M-$2.5M purchase, plus $50,000-$80,000 in reserves to fund the first 12-18 months of negative monthly cash flow while the property stabilizes with a tenant. Investors with less capital depth or without stable outside income to fund the carrying cost should consider the central Valley markets in the PEP coverage area, where the capital requirement and the cash flow gap are both substantially smaller.

🎯 Bottom Line

Calabasas 91302 and 91372 reward a fundamentally different investor than the central Valley markets in the PEP coverage area. This is not a market for capital recycling through renovation arbitrage — it is a market for investors with genuine capital depth and a long hold horizon who want exposure to the most durable school-quality demand anchor and the most geographically constrained, appreciation-resilient single-family inventory in the western SFV/Santa Monica Mountains corridor. The monthly cash flow at current rates is negative for nearly every leveraged acquisition in this market, and investors need to underwrite that reality honestly — funding it from outside income or reserves as the cost of access to LVUSD-anchored rental demand and a historically strong appreciation trajectory — rather than discovering it as a surprise eighteen months into ownership.

The investors who succeed here are the ones who verify the specific things this market requires that the central Valley doesn't: binding wildfire insurance quotes before closing, confirmed LVUSD catchment for every target address, Mello-Roos and HOA financial health for planned communities, and a genuine commitment to a multi-year hold rather than a near-term capital recycling plan. Get those four things right, bring the capital depth this price point requires, and Calabasas can be one of the more durable long-run residential investment plays in the entire PEP SFV coverage area.

At Parkway Estate Properties, Roman's renovation and investment experience across the SFV — including the specific underwriting discipline that premium, geographically constrained markets like Calabasas require — means every investor conversation we have here starts with the honest numbers: real insurance quotes, real LVUSD verification, real carrying cost projections, and a real assessment of whether this specific investor's capital and timeline match what this specific market demands.

📩 Want to Analyze a Specific Calabasas Investment Opportunity?

Bring us the address and we'll run the complete underwriting — LVUSD verification, Mello-Roos and HOA review, a path to a binding insurance quote, and the honest cash flow and appreciation model — before you're in contract.

Contact Liana Shersher at Parkway Estate Properties: 📧 liana@parkwayestate.com · 📞 (818) 208-5881 · 🌐 parkwayestate.com 15021 Ventura Blvd., Ste. 510, Sherman Oaks, CA 91403

About the Authors

Liana Shersher Liana Shersher is a licensed real estate agent with Parkway Estate Properties Inc. and an Accredited Buyer's Representative (ABR) serving the San Fernando Valley — with a focus on Sherman Oaks, Encino, Tarzana, Woodland Hills, and Northridge (DRE# 02164224). Liana guides first-time homebuyers through every step of the purchase, from the first showing to the keys in hand, and represents move-up and repeat buyers across the Valley. For sellers, she builds the pricing and marketing strategy that positions a home to sell for top dollar, fast. Buyers and sellers work with Liana for clear communication, sharp local knowledge, and an agent who treats their goals like her own.

Roman Shersher Roman Shersher is the broker-owner of Parkway Estate Properties Inc. and a real estate investor with 18 years of experience in the San Fernando Valley (DRE# 01855095). Roman has personally led or co-led renovations on dozens of properties across the Valley, including recent projects in Northridge (91324) and Woodland Hills (91364). That hands-on renovation and investment experience shapes every pricing conversation and days-on-market strategy at Parkway — sellers get a realistic read on what improvements actually return at resale, and buyers get an expert eye on a home's true condition and upside.

Parkway Estate Properties, Inc. 15021 Ventura Blvd., Ste. 510, Sherman Oaks, CA 91403 · (818) 208-5881 · parkwayestate.com · Broker License #: 01873092 Equal Housing Opportunity. Information herein is general and not legal, tax, or financial advice. Consult qualified professionals for your specific situation.

Categories

Recent Posts

Broker | Realtor ® | License ID: 01873092

+1(818) 208-5881 | info@parkwayestate.com