What's the Biggest Mistake Sellers Make in Calabasas?

The biggest mistake Calabasas 91302 and 91372 sellers make is misreading which of the two Calabasas markets their home actually belongs to — and pricing, marketing, and negotiating as if it belongs to the other one. A core flatland LVUSD-anchored listing priced and presented like a premium-tier discretionary luxury sale leaves buyer urgency unaddressed and money on the table. A premium hillside listing priced and marketed as if it will move with the same competitive urgency as the flatland tier sits for 60+ days, accumulates DOM stigma, and ultimately sells for less than an honest premium-tier strategy would have produced from day one.

This single tier-misread mistake branches into the five specific errors that actually cost Calabasas sellers money: pricing against the wrong comp set, under-disclosing the wildfire and HOA conditions that this specific buyer pool researches more aggressively than any other PEP coverage market, over- or under-investing in pre-sale preparation relative to the tier, mismanaging the negotiation when extended DOM has already signaled motivation, and choosing representation based on the most optimistic price quote rather than verified Calabasas-specific transaction performance. This article covers all five with the Calabasas-specific mechanics that make them costly here in particular.

1. 🚨 Mistake #1 — Misreading Your Tier

The single most consequential mistake a Calabasas seller can make happens before a single photo is taken or a single dollar is spent on preparation: misunderstanding which of Calabasas's two distinct markets their specific home actually competes in, and building a pricing and marketing strategy for the wrong one.

The Calabasas tier-misread mistake — a core flatland 91302 listing, anchored by Las Virgenes Unified School District demand, requires a fundamentally different pricing and marketing approach than a premium hillside listing competing for a thinner, more discretionary buyer pool. Sellers who apply the wrong tier's playbook consistently underperform what the correct strategy would have produced.

The Calabasas tier-misread mistake — a core flatland 91302 listing, anchored by Las Virgenes Unified School District demand, requires a fundamentally different pricing and marketing approach than a premium hillside listing competing for a thinner, more discretionary buyer pool. Sellers who apply the wrong tier's playbook consistently underperform what the correct strategy would have produced.

How this mistake happens in each direction:

Core flatland sellers who over-treat their listing as a luxury discretionary sale:

A $1.45M core flatland 91302 home is competing primarily for the LVUSD-motivated family buyer — a buyer pool that has remained deep and steady through 2025–2026 even as the premium tier has softened. Sellers in this tier who price defensively (anticipating buyer hesitation that this specific buyer pool generally doesn't display), who build in a long negotiation runway expecting the extended DOM patterns the premium tier has shown, or who market the home toward the discretionary lifestyle buyer rather than the school-motivated family are misallocating their marketing dollars and their pricing strategy against a buyer pool that doesn't behave that way.

The cost: a correctly priced, correctly marketed core flatland listing in 2026 is closing in 20–35 days at 97–102% of list. Sellers who misjudge this tier and price defensively below what the LVUSD-anchored demand actually supports leave money on the table; sellers who misjudge it by overpricing in anticipation of a competitive multiple-offer scenario that doesn't fully materialize accumulate unnecessary DOM in a tier where it isn't typical.

Premium and hillside sellers who expect flatland-tier urgency:

A $2.1M hillside 91302 listing is competing for a meaningfully thinner, more rate-sensitive, more discretionary buyer pool. Sellers in this tier who price at the top of their comp range expecting the same kind of buyer urgency that the core tier produces, who decline early offers below asking assuming a stronger offer is imminent, or who resist seller-paid buydown conversations because "that's not how this used to work" are applying a flatland-tier mental model to a market that is currently operating under different rules.

The cost: this is the mistake that produces the 60–80+ day DOM and the eventual 8–12% discount-to-original-list closes that frustrate premium-tier Calabasas sellers in 2026. A seller who recognizes the tier's actual current conditions from day one — pricing at the comp-supported midpoint rather than the aspirational top, proactively offering buydown flexibility, and engaging seriously with early offers — consistently closes faster and at a higher net price than the seller who holds out for flatland-tier dynamics that this tier isn't currently producing.

The correction:

Before setting any price, run the comp set specifically for your home's tier and sub-neighborhood — not a blended Calabasas-wide average that obscures which market you're actually in. A listing agent with verified recent closings in both the core flatland and the premium/hillside tiers should be able to tell you precisely which dynamics apply to your specific home before you commit to a strategy.

2. 📋 Mistake #2 — Under-Disclosing Wildfire, Mello-Roos, and HOA Conditions

The Calabasas buyer pool researches fire hazard status, insurance availability, special assessments, and HOA financial health more aggressively and more knowledgeably than buyers in any other PEP coverage market — and sellers who under-disclose these items, whether through omission or through minimizing language, are setting up the exact inspection-period and escrow-stage renegotiation that proactive disclosure would have avoided entirely.

Why Calabasas buyers research this more than buyers elsewhere:

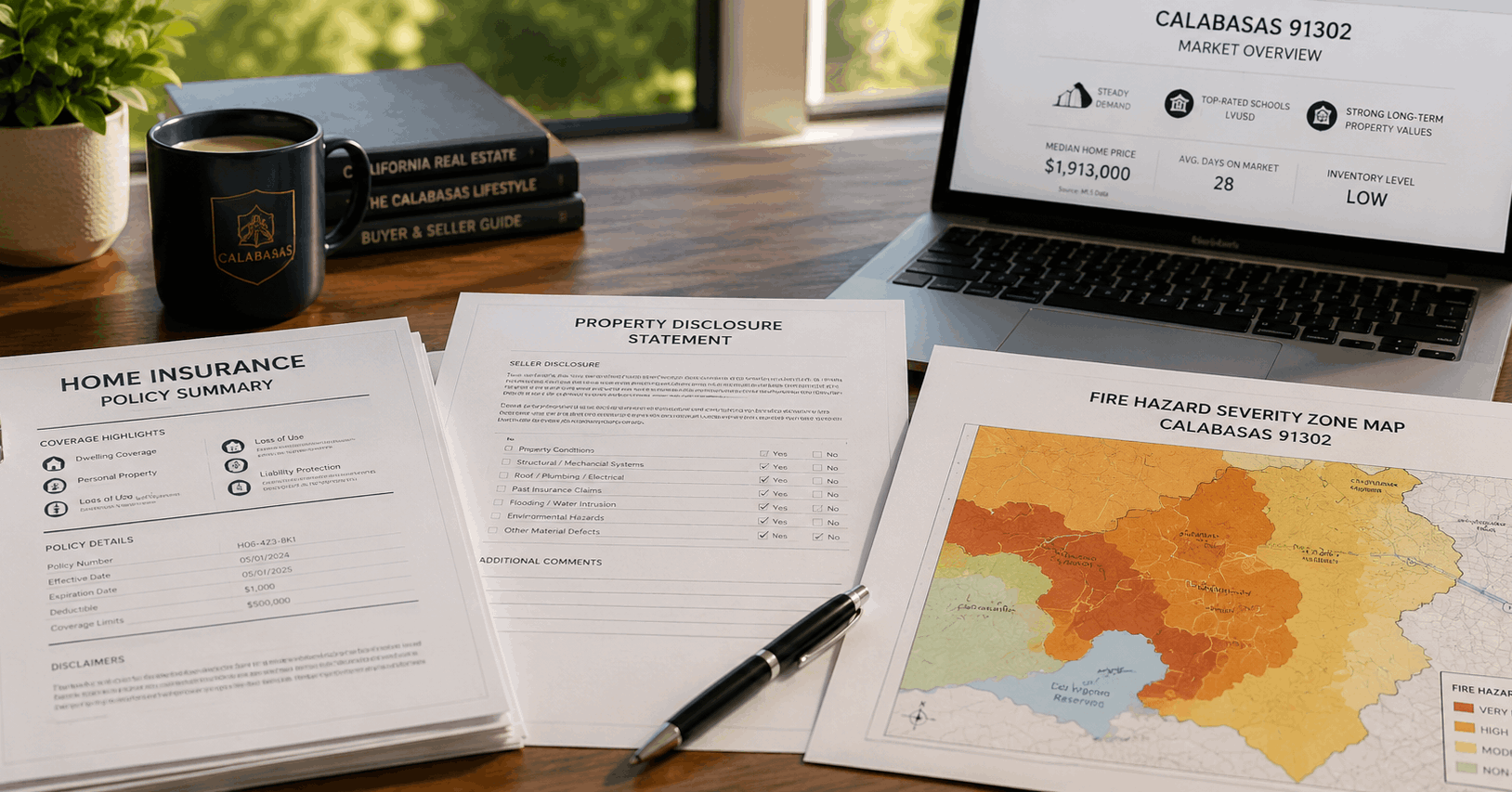

The combination of significant Very High Fire Hazard Severity Zone exposure across portions of 91302 and 91372, the prevalence of Mello-Roos financing in master-planned sections, and the common presence of HOA-governed communities means that a meaningful share of Calabasas buyers — and nearly all buyers working with an experienced agent — pull the Cal Fire FHSZ viewer, request a homeowner's insurance quote, and review HOA financials as a standard part of their evaluation before they ever submit an offer. This is not optional advanced diligence in this market; it is baseline buyer behavior.

The specific disclosure failures that cost Calabasas sellers:

- → 🔥 Minimizing or failing to disclose VHFHSZ status and prior insurance difficulty: A seller who knows their property has had insurance non-renewal notices, has been placed with the California FAIR Plan, or sits in a VHFHSZ zone and doesn't disclose this clearly is setting up a buyer discovery — during their own insurance shopping process — that arrives with maximum negotiating leverage in the buyer's favor, because the buyer now knows the seller didn't volunteer it.

- → 📝 Failing to disclose Mello-Roos obligations clearly: Mello-Roos assessments appear on the property tax bill, but sellers who don't proactively explain the specific annual amount and its duration leave buyers to discover it mid-escrow via their own title and tax research — a discovery that reads as a withheld cost rather than a known and disclosed one, even though it was technically always discoverable.

- → 🏛️ Providing outdated or incomplete HOA documents: For Calabasas properties in HOA-governed communities, sellers are obligated to provide current HOA financial statements, reserve studies, and disclosure of any pending special assessments. Sellers who provide stale documents, or who don't proactively flag a known pending assessment, create exactly the kind of late-discovery problem that produces buyer retreat or aggressive renegotiation in the final stretch of escrow.

What proactive disclosure produces instead:

- → ✅ A seller who discloses VHFHSZ status, current insurance carrier and premium, and any FAIR Plan dependency upfront — with documentation — allows buyers to factor the real cost into their offer from the start, rather than discovering it as a negotiating opportunity mid-escrow

- → ✅ A seller who provides a clear, written Mello-Roos summary (amount, expiration date if applicable, what it funds) alongside the disclosure package demonstrates good faith that buyers and their agents notice and respond to favorably

- → ✅ A seller who proactively provides current HOA financials and flags any known pending assessments removes the single most common cause of late-escrow Calabasas transaction friction

3. 🔨 Mistake #3 — Miscalibrating the Renovation Budget to the Wrong Scale

Calabasas sellers make this mistake in both directions, and both versions are costly: treating a Calabasas renovation decision with central-Valley-scale thinking (under-investing relative to what this market's buyer expects), or treating it with unconstrained ultra-luxury thinking (over-investing relative to what the specific sub-neighborhood's comp ceiling will actually absorb).

A Calabasas-appropriate renovation scope in progress — quality finishes that meet this market's buyer expectation without exceeding what the specific sub-neighborhood's comp ceiling will support. Calibrating this correctly, in either direction, is one of the most financially consequential preparation decisions a Calabasas seller makes.

A Calabasas-appropriate renovation scope in progress — quality finishes that meet this market's buyer expectation without exceeding what the specific sub-neighborhood's comp ceiling will support. Calibrating this correctly, in either direction, is one of the most financially consequential preparation decisions a Calabasas seller makes.

The under-investment version:

A seller who has read about the focused $30,000–$55,000 preparation scopes that work in Reseda or Lake Balboa and applies that same budget to a Calabasas listing will produce a home that reads as under-prepared to this market's buyer pool. Calabasas buyers at $1.4M+ expect kitchen and bath finishes, flooring quality, and overall presentation that a central-Valley-calibrated budget simply does not produce. A $35,000 "focused scope" kitchen refresh that would impress a Reseda buyer reads as dated and insufficient to a Calabasas buyer comparing it against other listings in their search with genuinely premium finishes.

The over-investment version:

The opposite mistake is equally costly: a seller who assumes that because Calabasas is a luxury market, any level of renovation spend will be recovered at sale. A seller who invests $280,000 in an ultra-premium kitchen and primary suite renovation on a home whose specific sub-neighborhood comp ceiling tops out at $1.65M has spent well beyond what that ceiling can return — the renovation doesn't lift the comp ceiling itself, and the seller absorbs the excess as a sunk cost rather than a recovered investment.

The correct calibration process:

- → ✅ Pull the specific sub-neighborhood comp ceiling first — not a Calabasas-wide average, but closed sales within 0.4 miles, comparable bedroom/bathroom count, comparable lot size, in the last 90–120 days

- → ✅ Identify the gap between as-is value and the renovated comp ceiling for that specific sub-neighborhood — this gap, not a generic renovation budget rule of thumb, is what determines how much investment can be profitably recovered

- → ✅ Calibrate finish quality to the buyer pool actually shopping that price point — a $1.5M core flatland listing requires quality, current finishes (think well-executed mid-to-upper-range, not ultra-custom); a $2.3M hillside listing competing for a more discerning buyer may support and require a higher finish tier to reach its full comp ceiling

- → ✅ Get the contractor bids from operators with verified Calabasas-scale project experience — a contractor whose pricing and finish-quality calibration comes from central Valley work will under-spec a Calabasas project; a contractor whose experience is exclusively ultra-luxury Hidden Hills or Bel Air work may over-spec one

4. 🤝 Mistake #4 — Failing to Recognize and Act on Buyer Motivation Signals

Once a Calabasas listing — particularly a premium or hillside listing — has accumulated meaningful days on market, it has already done something valuable that sellers frequently fail to recognize: it has filtered down to a buyer pool that is genuinely serious, comp-literate, and specifically interested in that property despite its extended exposure. The mistake is treating every offer that arrives after week six or eight with the same posture a seller would have used in week one, rather than recognizing that the negotiating dynamic has shifted.

What changes after extended DOM:

- → 📊 The remaining interested buyers have already done the comp work. Anyone touring or making an offer on a Calabasas listing at day 50 has almost certainly already seen the DOM, asked their agent why it's still on the market, and run their own comp analysis. They are not naive offers — they are calculated ones, and they deserve a serious, calculated response rather than a reflexive rejection.

- → 📊 Holding firm on original pricing after 45+ days sends a specific signal. A seller who refuses to engage seriously with a comp-grounded offer at day 55, insisting the home is worth the original list price, is implicitly arguing that the market's response over the prior eight weeks was wrong — a position that is rarely correct and that experienced buyer's agents will recognize and respond to by simply moving their client to the next listing.

- → 📊 The cost of "waiting for a better offer" compounds. Each additional month of carrying cost on a $1.8M–$2.5M Calabasas property — mortgage, property tax, insurance, HOA, maintenance — runs $8,000–$14,000/month. A seller who declines a reasonable, comp-supported offer at day 50 hoping for a stronger one at day 80 is betting that 30 additional days of carrying cost and continued market exposure will produce a materially better outcome than engaging seriously now.

The correct response to extended-DOM offers:

- → ✅ Treat any offer arriving after 30+ days of DOM as a serious negotiation starting point, not an opening insult to be dismissed

- → ✅ Counter with specific, comp-grounded reasoning rather than a flat restatement of the original asking price

- → ✅ Consider non-price concessions — seller-paid buydown contributions, closing cost credits, flexible timing — as tools that can bridge a gap without requiring the seller to publicly reduce their stated price

- → ✅ Recognize that the buyer who has been watching your listing for six weeks and finally made an offer is more likely to close than a hypothetical future buyer who hasn't appeared yet

5. 🧭 Mistake #5 — Choosing the Agent Who Quoted the Highest Price

This mistake exists in every PEP coverage market, but it carries a specific and larger cost in Calabasas because the dollar amounts involved make even a modest percentage misjudgment a substantial absolute loss, and because correctly distinguishing between the core flatland and premium tiers — the foundation of Mistake #1 — requires demonstrated knowledge that not every agent quoting a Calabasas listing actually has.

The Calabasas agent selection conversation, done correctly — grounded in verified recent transaction performance across both the core flatland and premium/hillside tiers, rather than the highest available list-price quote. At Calabasas price points, the gap between accurate and inflated pricing represents a meaningfully larger absolute dollar cost than in lower-priced PEP coverage markets.

The Calabasas agent selection conversation, done correctly — grounded in verified recent transaction performance across both the core flatland and premium/hillside tiers, rather than the highest available list-price quote. At Calabasas price points, the gap between accurate and inflated pricing represents a meaningfully larger absolute dollar cost than in lower-priced PEP coverage markets.

Why this mistake is more expensive in Calabasas specifically:

The same agent-incentive dynamic that exists everywhere — quoting an above-market price to win the listing, knowing the price-reduction conversation will happen later — produces a larger absolute dollar cost here. An 8% overpricing error on a $700,000 central Valley home is a $56,000 miscalibration; the same 8% error on a $2,000,000 Calabasas home is a $160,000 miscalibration, with proportionally larger carrying costs accumulating during the inevitable correction period.

What to evaluate instead of the price quote:

- → ✅ Verified recent closings specifically in your tier. An agent with strong recent core flatland closings may not have current premium/hillside transaction experience, and vice versa — ask specifically about closings in your home's actual price band and sub-neighborhood within the last 12 months.

- → ✅ Specific articulation of which tier your home falls into and why. An agent who can clearly explain, with comp data, whether your home is competing in the LVUSD-anchored core market or the more discretionary premium market — and what that means for pricing and timeline expectations — has demonstrated the market-specific knowledge this article has covered throughout.

- → ✅ A clear, documented plan for wildfire and HOA disclosure. Does the agent proactively recommend obtaining a current insurance quote and HOA financial documents before listing, or do they treat these as items to address only if a buyer asks? The correct answer is always proactive.

- → ✅ Calibrated, comp-grounded renovation or preparation guidance — not a generic "stage it and clean it up" recommendation, but a specific scope grounded in your home's actual sub-neighborhood comp ceiling.

🚫 What NOT to Overdo

Don't assume every Calabasas sub-neighborhood behaves like the one you've heard about. A seller whose neighbor in a different 91302 sub-neighborhood sold quickly in a multiple-offer situation may conclude their own home — in a different tier, with different fire-zone exposure, in a different school catchment pocket — should behave the same way. Calabasas's two-tier structure described throughout this article is itself a simplification; within each tier, specific sub-neighborhoods have their own comp ceilings and buyer pool characteristics that deserve individual analysis rather than a borrowed assumption from a neighbor's experience.

Don't treat wildfire disclosure as a negotiating weakness to minimize. Some Calabasas sellers approach VHFHSZ and insurance disclosure as something to soften or delay because they fear it will scare buyers away or invite price pressure. In a market where buyers are going to discover this information regardless — through their own Cal Fire research, their own insurance shopping, or their own agent's standard diligence — proactive, clear disclosure consistently produces better outcomes than a buyer's mid-escrow discovery of information the seller appeared to be withholding.

Don't over-correct into excessive renovation spend because "Calabasas is luxury." The luxury market positioning of Calabasas does not mean unlimited renovation spend is automatically recovered. Every renovation decision should be tested against the specific sub-neighborhood's comp ceiling before committing capital, exactly as in every other PEP coverage market — the only difference here is the absolute dollar scale of the numbers involved, which makes the cost of skipping this discipline larger, not smaller.

Don't confuse a single low offer early in the listing period with the kind of motivated, comp-grounded offer that arrives after extended DOM. Mistake #4's guidance about taking later offers seriously is not an instruction to accept every lowball offer that arrives in week one before the market has had a chance to respond. The distinction matters: an unreasonably low offer in the first week of a fresh, well-prepared listing is a different signal than a reasonable, comp-supported offer arriving after eight weeks of genuine market exposure.

Don't let agent selection become primarily a negotiation over commission rate. While commission structure is a legitimate conversation, Calabasas sellers who select representation primarily on the basis of the lowest commission percentage, without equally weighing verified tier-specific transaction performance and disclosure discipline, frequently end up with the same costly outcomes described throughout this article delivered by a less expensive but less effective representation.

🏠 Real-World Scenario — Calabasas 91302

A seller in the core flatland tier of 91302 — a well-maintained 4-bedroom, LVUSD-verified, in original-to-lightly-updated condition — interviewed three agents before listing. The first quoted $1.72M, citing two premium-tier sales from a different, more discretionary sub-neighborhood as comps. The second quoted $1.58M with a clear, sub-neighborhood-specific comp set drawn from four recent core flatland closings. The third quoted $1.49M, erring conservative to guarantee a fast sale and an easy commission.

We ran the seller's own comp analysis using only verified core flatland 91302 closings within 0.4 miles in the prior 90 days: the data supported $1.56M–$1.61M, closely matching the second agent's analysis and well below the first agent's optimistic comp set drawn from the wrong tier.

The seller chose the second agent specifically because the comp work demonstrated correct tier identification rather than either inflated optimism or excessive conservatism. They listed at $1.595M. First week: 11 showings, reflecting the steady LVUSD-anchored demand this tier has shown through 2026. Two offers by day 16, one at $1.585M and one at $1.605M with a 2-1 seller-credit request. They accepted the higher offer with a modest credit concession, closing at an effective $1.594M — within 1% of their initial comp-grounded estimate.

The seller's retrospective: had they listed with the first agent at $1.72M — pricing for the wrong tier — they would likely have spent 6–10 weeks accumulating DOM before reducing to approximately the same $1.59M–$1.61M range the correct analysis identified from day one, having lost the first-week showing momentum and absorbed unnecessary carrying costs in the process.

🏠 Real-World Scenario — Calabasas 91302

A seller in a hillside 91302 sub-neighborhood listed a 5-bedroom view property at $2.45M based on an agent's quote that emphasized the property's view premium and the "the right buyer will pay for this" framing common in ultra-discretionary luxury sales. The seller had owned the home for 19 years, had no specific timeline pressure, and was comfortable waiting for what the agent described as "the perfect buyer."

Sixty-eight days in: four showings total, no offers, and a listing agent who continued to advise patience. The seller had not disclosed, nor had the listing materials mentioned, that the property's specific street segment carried VHFHSZ designation and that the seller's own insurance had moved to FAIR Plan coverage three years earlier at a meaningfully elevated premium.

We were engaged for a second opinion at day 70. The comp analysis for this specific hillside sub-neighborhood, incorporating the current jumbo-rate-affected premium-tier buyer pool described in this market's broader 2026 conditions, supported a value closer to $2.21M–$2.27M — not the $2.45M original list. We also identified that the undisclosed FAIR Plan history was a near-certain discovery point for any serious buyer's own insurance shopping, and recommended proactive disclosure with current premium documentation rather than waiting for a buyer to find it.

We relisted at $2.265M with full proactive disclosure of the fire zone status, the FAIR Plan history, and a current insurance quote already in hand for prospective buyers' reference. First week post-relaunch: 7 showings — nearly double the total the prior 68 days had produced — from buyers who appreciated not having to chase down the insurance information themselves. An offer arrived at day 9 at $2.235M; after one round of negotiation, the parties settled at $2.25M, closing 34 days after the relaunch.

Total outcome: a sale at $2.25M roughly 80 days after the original listing's relaunch, versus a prior 68 days of zero offers at $2.45M. The combination of tier-appropriate pricing and proactive fire/insurance disclosure produced in five weeks what the original strategy had failed to produce in over two months.

❓ FAQ

Why do Calabasas homes sometimes take so long to sell? Extended days on market in Calabasas almost always traces to one of two causes: pricing the home against the wrong tier's comp set (typically pricing a premium or hillside property as if the deeper, faster-moving core flatland demand applies to it), or under-disclosed wildfire, Mello-Roos, or HOA conditions that surface during buyer due diligence and stall or derail otherwise-interested buyers. Correctly tiered pricing combined with proactive disclosure of fire zone and HOA conditions consistently produces faster sales than either factor addressed in isolation.

What is the biggest mistake Calabasas sellers make? Misreading which of Calabasas's two markets — the LVUSD-anchored core flatland tier or the more discretionary, currently softer premium and hillside tier — their specific home actually belongs to, and pricing or marketing it according to the wrong tier's dynamics. This single misjudgment is the root cause behind most of the pricing, timeline, and negotiation problems Calabasas sellers experience.

Should I disclose wildfire risk before listing my Calabasas home? Yes, proactively and with documentation. Calabasas buyers — more than buyers in most comparable markets — independently research Fire Hazard Severity Zone status, insurance availability, and FAIR Plan dependency before or during their property evaluation. Sellers who disclose this information clearly upfront, ideally with a current insurance quote already in hand for buyer reference, consistently fare better than sellers whose buyers discover this information independently mid-escrow and treat it as a withheld fact rather than a known and disclosed condition.

How much should I spend preparing my Calabasas home for sale? The correct renovation or preparation budget depends entirely on your specific sub-neighborhood's comp ceiling, not on a generic "luxury market" assumption that any spend will be recovered, nor on a central-Valley-calibrated budget that under-delivers relative to what Calabasas buyers expect. Pull closed comps within 0.4 miles in the last 90–120 days, identify the gap between your as-is value and the renovated ceiling for that specific tier and sub-neighborhood, and calibrate your investment to that gap rather than to an assumed market-wide budget.

Should I accept an offer that comes in after my Calabasas listing has been on the market a long time? Generally yes, with serious engagement rather than reflexive dismissal. An offer arriving after 30+ days of genuine market exposure, particularly in the premium and hillside tier, typically comes from a comp-literate buyer who has done real homework — it deserves a counter grounded in current comp data rather than a flat restatement of the original list price. Holding out for a hypothetical stronger future offer while declining a reasonable current one compounds carrying costs and frequently produces a worse eventual outcome.

How do I choose the right listing agent for my Calabasas home? Evaluate agents on verified recent closings specifically within your home's price tier and sub-neighborhood — not a Calabasas-wide track record that may be concentrated in a different tier than yours. Ask the agent to clearly articulate which tier your home competes in and why, request their specific plan for proactive wildfire and HOA disclosure, and be wary of any quote significantly above what your own comp research supports, since the gap between accurate and inflated pricing represents a larger absolute dollar cost in Calabasas than in lower-priced markets.

🎯 Bottom Line

The biggest mistake Calabasas sellers make is not a single bad decision — it is the foundational misjudgment of which Calabasas market their home actually belongs to, compounded by the disclosure shortcuts and renovation miscalibrations that follow from not having done that diagnosis correctly. The core flatland tier, anchored by Las Virgenes Unified School District demand, behaves like a steady, competitive family market that rewards correct pricing and decisive preparation. The premium and hillside tier, in 2026, behaves like a genuinely negotiable market that rewards realistic pricing, proactive disclosure, and serious engagement with motivated buyers rather than the aspirational holdout that worked in a different rate environment.

Sellers who get the tier diagnosis right, who disclose wildfire and HOA conditions proactively rather than reactively, who calibrate their preparation spend to their specific sub-neighborhood's comp ceiling, and who engage seriously with comp-grounded offers once their listing has done the work of attracting a genuine buyer — those sellers consistently outperform the ones who skip any one of these steps, regardless of which tier they're selling in.

At Parkway Estate Properties, every Calabasas seller conversation starts with the tier diagnosis, because every other decision in this market follows from getting that first one right. Liana's representation across Calabasas 91302/91372 and the broader SFV means every pricing recommendation reflects verified, tier-specific recent transaction data, not an optimistic blended average. Roman's renovation experience means every preparation recommendation is calibrated to what your specific sub-neighborhood's comp ceiling will actually return.

📩 Want an Honest Read on Which Calabasas Market Your Home Actually Competes In?

We'll run the sub-neighborhood-specific comp analysis, identify your home's correct tier, and give you the disclosure checklist and preparation scope that produces the strongest outcome for your specific property — before you commit to any pricing strategy.

Contact Liana Shersher at Parkway Estate Properties: 📧 liana@parkwayestate.com · 📞 (818) 208-5881 · 🌐 parkwayestate.com 15021 Ventura Blvd., Ste. 510, Sherman Oaks, CA 91403

About the Authors

Liana Shersher Liana Shersher is a licensed real estate agent with Parkway Estate Properties Inc. and an Accredited Buyer's Representative (ABR) serving the San Fernando Valley — with a focus on Sherman Oaks, Encino, Tarzana, Woodland Hills, and Northridge (DRE# 02164224). Liana guides first-time homebuyers through every step of the purchase, from the first showing to the keys in hand, and represents move-up and repeat buyers across the Valley. For sellers, she builds the pricing and marketing strategy that positions a home to sell for top dollar, fast. Buyers and sellers work with Liana for clear communication, sharp local knowledge, and an agent who treats their goals like her own.

Roman Shersher Roman Shersher is the broker-owner of Parkway Estate Properties Inc. and a real estate investor with 18 years of experience in the San Fernando Valley (DRE# 01855095). Roman has personally led or co-led renovations on dozens of properties across the Valley, including recent projects in Northridge (91324) and Woodland Hills (91364). That hands-on renovation and investment experience shapes every pricing conversation and days-on-market strategy at Parkway — sellers get a realistic read on what improvements actually return at resale, and buyers get an expert eye on a home's true condition and upside.

Parkway Estate Properties, Inc. 15021 Ventura Blvd., Ste. 510, Sherman Oaks, CA 91403 · (818) 208-5881 · parkwayestate.com · Broker License #: 01873092 Equal Housing Opportunity. Information herein is general and not legal, tax, or financial advice. Consult qualified professionals for your specific situation.

Categories

Recent Posts

Broker | Realtor ® | License ID: 01873092

+1(818) 208-5881 | info@parkwayestate.com